What Does Dave Ramsey Mean by “Growth Stock Mutual Funds” and Why It’s Scary

Cash Flow and Budgeting Investments RetirementI’m a Dave Ramsey fan. After reading “Financial Peace Revisited”, my wife and I worked hard and eliminated our student loans and a car loan in 18 months. We pumped up our emergency fund and are now on to baby steps 4 and 5 – invest 15% of household income for retirement and college funding for the kids. I’ve also listened to his radio show, read numerous additional books by Dave and Chris Hogan, and have listened regularly to Podcasts by Chris Hogan, Ken Coleman, and Rachel Cruze (all Ramsey Solutions personalities). My family wouldn’t be financially where it is today without Uncle Dave.

Even with all of the exposure to Dave’s materials, there’s one thing that always confused me. When I got to baby step 4 and I was ready to start saving for retirement, I understood his suggestion to use mutual funds (i.e. don’t put all your eggs in one basket). However, I didn’t get what he meant by dividing your mutual fund investments equally between the “four good growth stock mutual fund categories – growth, growth and income, aggressive growth, and international.” International makes sense. It’s most likely mutual funds that hold stocks from outside the US. But, the other 3 categories I could only guess at. Even after becoming a financial advisor it still didn’t make sense.

This week I sat down and did a little research in hopes of understanding what those categories mean.

First a disclaimer: The content of this post is provided for discussion purposes only, and should not be misconstrued as investment advice. Under no circumstances does this information represent a recommendation to buy or sell securities.

First Guess

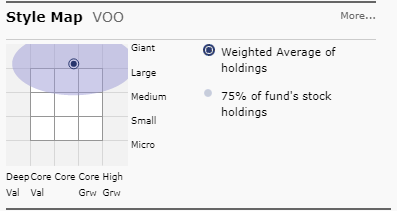

My first guess was that Dave’s categories corresponded with Morningstar’s Style Map. The Style Map is a grid that visually indicates the investment style of a mutual fund or other investment vehicle. For example, here is the Morningstar Style Map for the Vanguard S&P 500 ETF (ticker VOO):

If you follow the grid lines VOO sits in the Giant Core category.

Just guessing, I assumed Dave’s “Growth and Income” corresponded with Morningstar’s “Value” category represented as “Val” on the chart above. Morningstar defines Morningstar’s “Value” category as including investments with “low price ratios and high dividend yields”. Mutual funds designed to have high dividend yields often have “Income” in the fund name to attract investors seeking regular inflows of dividends. For example, Vanguard Equity Income Fund Investor Shares (VEIPX) and Fidelity Equity Income Fund (FEQIX) both fall into the Core Value category on Morningstar’s Style Map. So, assuming “income” equates to “value”, then Dave’s Categories would correspond to the Morningstar Style map as follows:

- Growth = Core

- Growth and Income = Value

- Aggressive Growth = Growth

What They Really Mean

When I did a little more searching, I found that I was right and wrong at the same time. Dave’s advice does correspond with Moringstar’s Style Map. However, Dave’s categories actually correspond with the other Morningstar Style Map categories – Large, Medium, and Small market capitalization.

There is a blog post on Dave Ramsey’s website where a financial advisor named Brant Spesshardt explains what each category means. Here are the corresponding categories and the Morningstar chart for illustrative purposes:

- Growth and Income = Core Large

- Growth = Core Medium

- Aggressive Growth = Core Small

- International = Non-US

Dave’s recommendation is to have 25% of your invested assets in each of these four categories. Learning this is surprising to say the least. One of the reasons that he often tells his listeners to get rid of debt is the risks associated with holding debt. With debt you have monthly payments that you have to make. If your income drops, you still have to make the payments. You end up with less money for other essentials like food, utilities, etc. However, his suggested investment strategy is honestly, quite risky. If you follow all of his advice, you won’t have any debt, but you may not have enough income in retirement either.

Too Risky

To show you how risky this would be, I created a portfolio using mutual funds from the Vanguard family of funds that fit neatly into Dave’s four categories:

- Growth and Income = Vanguard 500 Index Fund (VFINX)

- Growth = Vanguard Mid Cap Index Fund (VIMSX)

- Aggressive Growth = Vanguard Small Cap Index Fund (NAESX)

- International = Vanguard Total International Stock Index Fund (VGTSX)

I then ran the investments through a historical analysis program to see what they would have done over time. The maximum drawdown (i.e. how deep is the deepest plunge the investments took) on the above listed investments from 1986 (the earliest time period available based on real historical data) until today is negative 54.04%!!!!

That seems like a big number, but what would that do to your money? Imagine it’s 2007. You’ve been religiously saving money for retirement since you started your first “real” job in 1972 at age 30. You’ve had a good 35 years in pharmaceuticals and you’re ready to hang up your hat. Your $1.5 million nest egg will allow you to draw $60,000 a year from your IRA for income replacement. You also plan to draw social security. You’ve followed Dave’s advice and you’ve got 25% of your investment in each “good growth stock mutual fund” categories. Then 2008 hits and over the course of a year your investments drop by $810,600.00. The $60,000 per year you could have safely drawn from your investments is now only $27,600 plus social security. Because of such an enormous loss, you pull your money out of the stock market and miss out on it’s total rebound that gradually occurs over the next two years. Now you’re stuck with your losses.

Give Dave Some Credit

I gotta give Dave credit where credit is due though. He’s helped millions of people get out of debt and clean up their finances, myself included. And, whenever he mentions investments, he advises his listeners to get in touch with a local financial advisor in order to get personalized investment advice. Also, he may be able to take a 54% drop in his investments. He has a huge business and millions of dollars of real estate that will continue to produce income for him in the event of a stock market downturn. If investments are only a portion of your total wealth you can financially afford to take greater risks for a bigger potential gain in the stock market.

However, the average American doesn’t have the luxury of taking such a big hit to the wallet and should think twice before following Dave’s investment advice. Talk to a reputable financial advisor in your area and get the personalized advice that Dave recommends. You can become financially confident and you can have a better investment experience.